Advertisement

Advertisement

The Inverse Connection Between Interest Rates And Bond Prices

Jan 01, 2025 By Kelly Walker

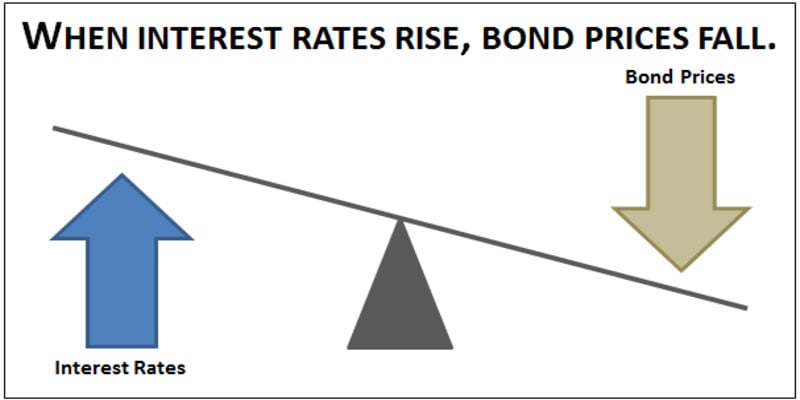

Investors can better comprehend the effect of interest rate changes on bond prices by understanding the inverse relationship between interest rates and bond prices, a fundamental concept in finance. It is a term used to describe how the general interest rate climate affects the market price of bonds. The value of bonds often decreases when interest rates rise, and increases as rates fall. Interest rates and bond prices are inversely related because bond prices are based on the present value of the bond's future cash flows (interest payments and the principal repayment at maturity).

We can determine the present value of these cash flows by discounting them at a rate consistent with the prevailing interest rate environment. The discount rate used to determine the present value of future cash flows increases in tandem with the level of interest rates. Bond prices fall because of the resulting decline in the current value of future cash flows. Bond prices rise when interest rates drop because a lower discount rate means a higher present value for future cash flows. Anyone looking to improve their portfolio's performance should familiarize themselves with the inverse link between interest rates and bond prices. Bond investors must factor this connection into their investment decisions since it has substantial ramifications.

How The Connection Works

We can learn the mechanics of the inverse relationship between interest rates and bond prices by analyzing bond price calculations. Future cash flows, such as interest payments and the principal payment at maturity, are discounted to arrive at the bond's price. We can determine the present value of these cash flows by ignoring them at a rate consistent with the prevailing interest rate environment. The discount rate used to determine the present value of future cash flows increases in tandem with the level of interest rates. Bond prices fall because of the resulting decline in the current value of future cash flows. Bond prices rise when interest rates drop because a lower discount rate means a higher present value for future cash flows.

Relationship Ramifications

Bond investors should consider the severe consequences of the inverse link between interest rates and bond prices. Bond investors will see a decline in their portfolio value as interest rates increase and bond prices fall. This is because the greater discount rate used to determine the present value of future cash flows will have decreased the market value of their bonds. Bond prices rise when interest rates fall, providing a positive return for bondholders even if bond prices rise by less than the change in interest rates.

Alterations in interest rates can affect bond yields and their direct effect on bond prices. Bond yield is the rate of return for buyers relative to the cost of the bond. Bond yields rise when bond prices fall due to interest rate hikes. This is because the investor is now getting the same quantity of interest payments but at a cheaper cost. Bond yields fall when bond prices rise due to declining interest rates, and vice versa.

Relationship Restrictions

While the idea that rising interest rates will lead to falling bond prices is a cornerstone of finance, its applicability is not without its caveats. The nonlinear nature of the connection is one of its drawbacks. This correlation is only sometimes straightforward; additional variables, including credit risk, inflation expectations, and market liquidity, may enter into play.

The fact that the connection could not be stable throughout all possible time frames is still another restriction. Changes in interest rates may have a more significant impact on bond prices in the short term. In contrast, changes in the issuer's credit quality or the economic climate may become more critical over time.

Conclusion

As a last thought, bond investors must understand the inverse link between interest rates and bond prices. Bond prices and the yields investors receive are susceptible to fluctuations in interest rates. The bond pricing mechanism at the heart of this connection is the discounting of future cash flows by an interest rate that reflects market conditions. Other factors, like credit risk, inflation expectations, and market liquidity, may influence the connection and make it nonlinear. For this reason, these considerations should not be overlooked by investors. Bond prices and interest rates tend to move in the opposite direction, so investors must remember this while making decisions and managing their bond portfolios.

How Venture Capitalists Make Investment Choices?

An Overview of the Vanguard Cash Reserves Federal Money Market Fund

The Inverse Connection Between Interest Rates And Bond Prices

10 Best Landlord Insurance Companies

How to Trade Orange Juice Options

Frac Sand Scarcity: Meeting the Growing Demand

Best Buy's Expanding Portfolio: Top 3 Subsidiary Companies

How to Calculate the Return on Investment (ROI) of a Marketing Campaign