Advertisement

Advertisement

Deciphering Contingent Convertibles (CoCos): Unveiling the Secret Saviors of Banks

Jan 23, 2025 By Kelly Walker

If you've ever ventured into the intricate realm of finance, chances are you've come across the term "Contingent Convertibles," or CoCos for brevity. Don't be daunted by the jargon; we're here to demystify it in plain language. Imagine CoCos as financial instruments with a superhero-like quality, poised to rescue banks in times of trouble, just like a caped crusader safeguarding a city's peace.

These unique financial tools aren't mere abstractions; they're the unsung heroes of the banking world, ready to step in and prevent financial disasters when needed most.

Breaking Down the Basics of CoCos

What Are CoCos, Anyway?

Contingent Convertibles, or CoCos, are hybrid financial instruments that combine features of bonds and stocks. Banks issue them and serve a unique purpose in the financial world. CoCos acts as a financial shock absorber for banks during times of crisis, helping them stay afloat when the going gets tough.

Understanding Their Dual Nature

CoCos are called "contingent" because they come with a special condition. They convert into common equity or are written off if certain predefined triggers are met. These triggers are usually related to the bank's financial health, such as a drop in its capital reserves. In simpler terms, CoCos can morph into stocks when a bank faces trouble, providing the bank with a capital boost.

The Risky Side of CoCos

Now, here's where things get interesting and a tad risky. CoCos are considered risky investments because their value and existence are tied to the bank's financial well-being. If the bank runs into severe financial trouble, the CoCos can be converted into stocks, resulting in losses for investors.

The Role of CoCos in Banking Stability

CoCos play a pivotal role in maintaining Banking Stability. They provide a financial cushion, ensuring banks remain resilient during economic turmoil. By converting into equity when needed, CoCos infuse crucial capital, preventing potential crises and safeguarding the broader financial system.

Why Do Banks Issue CoCos?

Banks issue CoCos to bolster their regulatory capital. You see, regulators require banks to maintain a certain level of capital to ensure they can withstand economic shocks and financial crises. CoCos helps banks meet these requirements while acting as a financial safety net.

CoCos: The Crisis Managers

A bank's capital can take a hit during a financial crisis or a severe downturn, making it vulnerable. This is where CoCos step in as unsung heroes. If the predefined triggers are met, CoCos convert into common equity, injecting fresh capital into the bank. This cash infusion helps the bank stay afloat and continue its operations, preventing a full-blown financial catastrophe.

Investors Beware: The Risk-Reward Dilemma

For investors, CoCos can be a bit of a double-edged sword. On one hand, they offer higher yields than traditional bonds, making them attractive. On the other hand, the risk of conversion into equity during a bank's crisis is ever-present, potentially leading to significant losses. It's like balancing on a seesaw, weighing the potential rewards against the lurking risks.

How Do CoCos Work?

Now that we've grasped the essence of CoCos let's dive into how these financial instruments operate.

CoCo Coupon Payments

Much like conventional bonds, Contingent Convertibles, or CoCos, adhere to a schedule of regular Coupon Payments to their investors. What sets CoCos apart and makes them alluring to income-seeking investors is that these payments tend to be more generous than those offered by typical bonds.

It's akin to a sweeter deal for investors seeking steady income, making CoCos a compelling choice in fixed-income investments.

The Trigger Mechanism

The intriguing aspect of CoCos lies in their innate trigger mechanism. When a bank's capital descends below a predetermined threshold, often set by regulatory guidelines, CoCos springs into action.

Their response hinges on the instrument's specific terms, which dictate two possible outcomes: transformation into common shares, bolstering the bank's capital, or total write-off, extinguishing their value. This built-in adaptability makes CoCos a dynamic tool for safeguarding a bank's financial health during turmoil.

Conversion to Common Equity

Conversion into common equity means that CoCo holders become shareholders of the bank. While this can help the bank's capital position, it dilutes the ownership of existing shareholders. This is why CoCos are sometimes seen as a last resort for banks, as they prefer not to dilute existing shareholders unless necessary.

The Written-Off CoCos

In the worst-case scenario, if a bank faces extreme financial distress, CoCos can be written off entirely. This means investors may lose their entire investment. It's a risk that makes CoCos unsuitable for risk-averse investors.

The Pros and Cons of CoCos

Pros

- High Yields: CoCos generally offer higher Coupon Payments than traditional bonds, making them appealing to income-seeking investors.

- Strengthening Banks: CoCos act as a safety net, helping banks maintain capital levels during crises, ultimately contributing to financial stability.

- Flexibility: They provide banks with a flexible way to manage their capital, adjusting to changing circumstances.

Cons

- High Risk: CoCos converting into equity or being written off is ever-present, leading to significant losses for investors.

- Complexity: CoCos can be complex financial instruments, making them less suitable for novice investors who may not fully understand their workings.

- Regulatory Scrutiny: CoCos are subject to strict regulatory oversight, and any changes in regulatory requirements can impact their value.

The Bottom Line on CoCos

Contingent Convertibles, or CoCos, are intriguing financial instruments that serve as a safety net for banks during turbulent times. While they offer higher yields than traditional bonds, they come with unique risks, primarily related to their conversion into equity or potential write-off.

CoCos can be an attractive option for investors if they are willing to take on the associated risks. However, due to their complexity and potential loss, they may not be suitable for everyone. It's essential to carefully assess your risk tolerance and investment goals before considering CoCos as part of your portfolio.

On this page

Breaking Down the Basics of CoCos What Are CoCos, Anyway? Understanding Their Dual Nature The Risky Side of CoCos The Role of CoCos in Banking Stability Why Do Banks Issue CoCos? CoCos: The Crisis Managers Investors Beware: The Risk-Reward Dilemma How Do CoCos Work? CoCo Coupon Payments The Trigger Mechanism Conversion to Common Equity The Written-Off CoCos The Pros and Cons of CoCos Pros Cons The Bottom Line on CoCos

Understanding the Art of Revenue Calculation in Business

Selling Shares Before the Ex-Dividend Date: Maximizing Returns

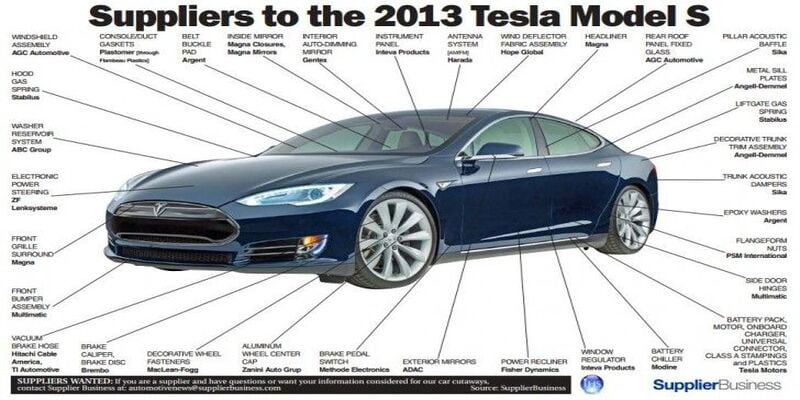

Who Are The Leading Suppliers For Tesla?

How Chime Makes Money

Review of Allstate Home Insurance

Net Profit Margin: An Overview

The Impact of CHIP on Children's Access to Healthcare Services

Difference between Fixed and Variable Deposit Interest Rates